A slow month in real estate feels personal.

You start checking your pipeline more.

You look at your bank account more.

You wonder if the leads are drying up.

You tell yourself the next closing will fix everything.

But the real problem is usually not the slow month.

The real problem is that you did not see it coming.

Most agents and small brokerages are great at chasing deals. They know how to follow up, show homes, negotiate, manage closings, and keep clients moving.

But when it comes to money, a lot of them are only looking at what already happened.

- A commission check came in.

- A bill went out.

- A card got charged.

- A closing got delayed.

- A tax payment came due.

Then suddenly the business feels tight.

That is not a strategy.

That is reacting.

The money lesson is simple:

You should not find out you are short when the money is already gone.

You need to know what is coming, what is going out, and how much cushion you have before the month gets ugly.

Simple explanation

Real estate income is not steady.

Some months are great.

Some months are quiet.

Some months look great on paper, but the money has not hit yet.

Some months have closings scheduled, but one inspection, appraisal, lender issue, or delayed title problem can push everything back.

That is why agents and small brokerages need to think ahead.

Not in a complicated way.

Just in a practical way.

You need to know:

- What closings are expected this month?

- What closings are expected next month?

- What commission checks are likely to come in?

- What splits, fees, and payouts will come out?

- What bills have to be paid no matter what?

- How much should be set aside for taxes?

- How much money is actually safe to use?

This matters because your business has two kinds of costs.

Some costs only happen when deals happen.

For example, if a deal closes, an agent may get paid. A referral partner may get paid. A transaction fee may come out. Those costs are tied to the deal.

But other costs happen whether you close anything or not.

- Software

- Rent

- Insurance

- Phone

- Marketing

- Website

- CRM

- Dues

- Assistant or admin help

Those bills do not care if your closing moved to next month.

They still hit.

That is why planning matters.

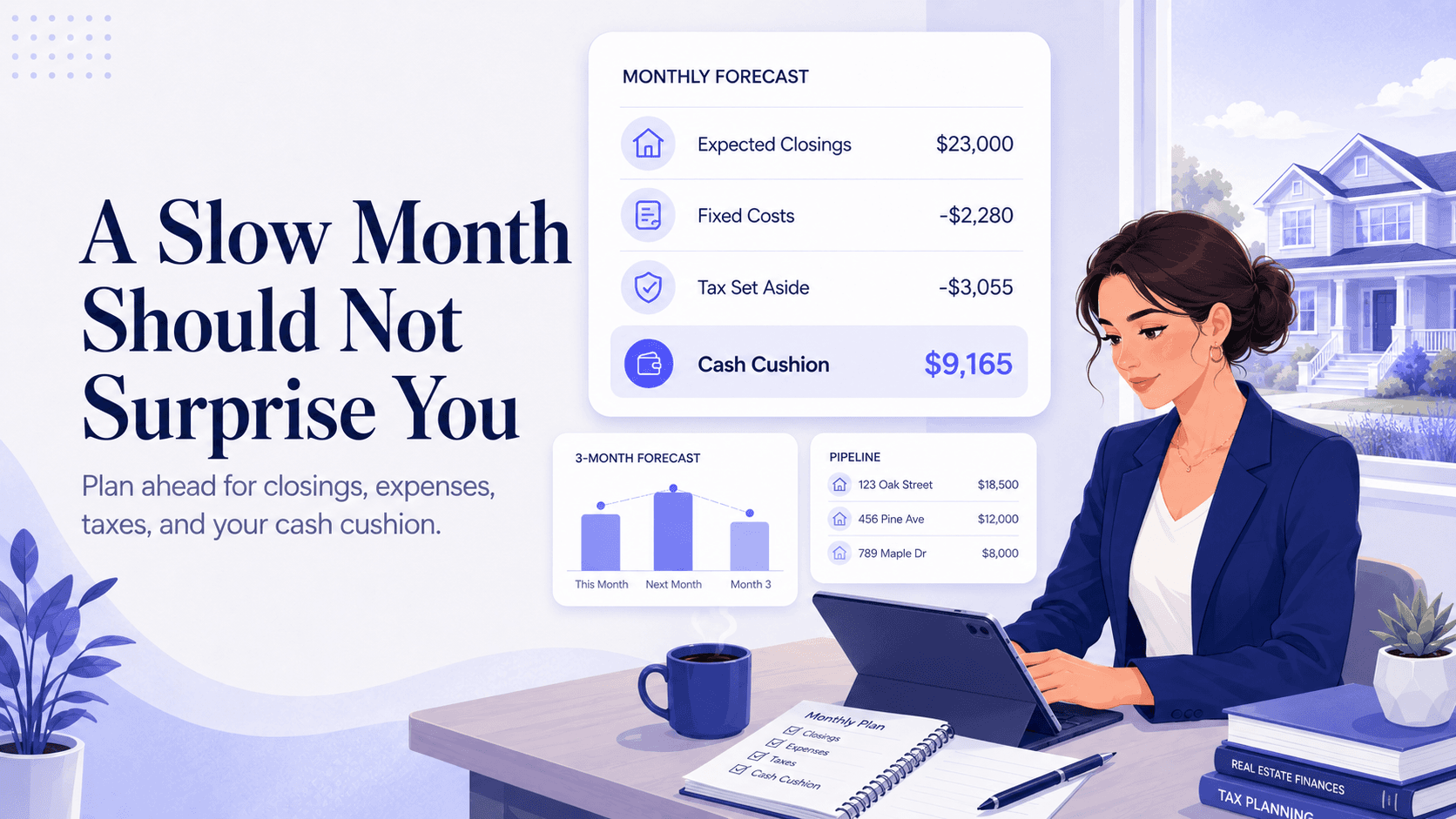

Example with numbers

Let’s say you are a solo agent going into June.

You have two expected closings.

- Closing 1 expected commission$9,000

- Closing 2 expected commission$14,000

- Total expected commission$23,000

That feels good.

But now you need to think about what will come out.

- Broker split$4,600

- Referral fee$2,000

- Transaction fees$700

- Listing and buyer expenses$1,200

- Total deal costs and payouts$8,500

Now you are down to:

$14,500

Then you have monthly business bills.

- CRM / software$250

- Phone / internet$180

- Marketing / ads$1,000

- Office or desk fee$500

- Dues / subscriptions$200

- Insurance$150

- Total fixed monthly costs$2,280

Now you are down to:

$12,220

Then you need to set aside taxes.

If you set aside 25% of what is left before taxes:

$3,055

Now the money you can actually work with is closer to:

$9,165

That is still a solid month.

But here is where real estate gets tricky.

What happens if Closing 2 gets delayed?

Now your expected commission drops from $23,000 to $9,000.

- Broker split on Closing 1$1,800

- Transaction fee$350

- Deal expenses$500

Now you are at:

$6,350

Your fixed monthly bills are still:

$2,280

Now you are at:

$4,070

Taxes still need to be set aside.

25% tax savings:

$1,017.50

Now your usable money is closer to:

$3,052.50

That is a very different month.

Nothing “bad” even happened.

One closing simply moved.

But if you were spending like both closings were guaranteed, you would feel the pain fast.

That is why you need to plan before the money hits.

The common mistake

The common mistake is counting pending closings like they are already paid.

Agents do this all the time.

They say, “I have $23,000 coming in this month.”

But you do not have $23,000 until the closing happens and the money clears.

Before that, you have expected money.

Expected money is useful for planning.

But it is dangerous for spending.

There is a huge difference between:

“I have two closings coming.”

And:

“I have enough money safely available after splits, fees, taxes, and monthly bills.”

That difference is what keeps you from getting blindsided.

Small brokerages have an even bigger version of this problem.

A broker may look at the pipeline and see several closings coming in. That looks strong.

But the brokerage also has agent payouts, rent, software, insurance, staff, transaction tools, lead costs, and other monthly costs.

If two or three closings move, the brokerage can feel tight even if the business is technically doing well.

That is why the question cannot just be:

“How much commission is coming in?”

The better question is:

“What happens if one or two closings move?”

That is the question that protects you.

How Kapytl helps

Kapytl helps agents and small brokerages stop flying blind month to month.

Instead of only looking backward at what already happened, Kapytl helps you see your money more clearly as you go.

You can track your commission checks, deal costs, fees, write-offs, receipts, and what is left in one place.

That gives you a clearer picture of where you stand before tax time, before your CPA asks, and before the slow month catches you off guard.

Kapytl helps you see:

Expected money

Commission checks, upcoming closings, referral income, and brokerage income.

Money going out

Splits, agent payouts, fees, software, marketing, insurance, dues, signs, photos, and other real estate costs.

Receipts and write-offs

The things agents forget until tax time.

What is actually left

The number that tells you whether you are safe, tight, or need to adjust.

For agents, this means you can stop treating every commission check like free money.

For small brokerages, this means you can see how your closings, payouts, and expenses affect the business before the bank account starts screaming at you.

The goal is not to make money more complicated.

The goal is to make it less surprising.

Because when you can see your numbers clearly, you can make smarter decisions.

- You can slow down spending before a slow month.

- You can build a cash cushion.

- You can plan for taxes.

- You can see which months are risky.

- You can stop assuming the next closing will fix everything.

That is how you keep more of what you make.

A slow month should not surprise you.

Kapytl helps real estate agents and small brokerages see what is coming in, what is going out, and what is actually left before the month gets tight.

Stop waiting for your bank account to warn you.

Start planning your real estate money with Kapytl.