Tax time should not be the moment you find out what you owe.

But for a lot of real estate agents, that is exactly when it happens.

You had a great year. The commissions came in. The money got spent. Then your CPA hands you a number that feels impossible.

The fix is simple: set the money aside before you ever touch it.

The only question is how much.

The short answer

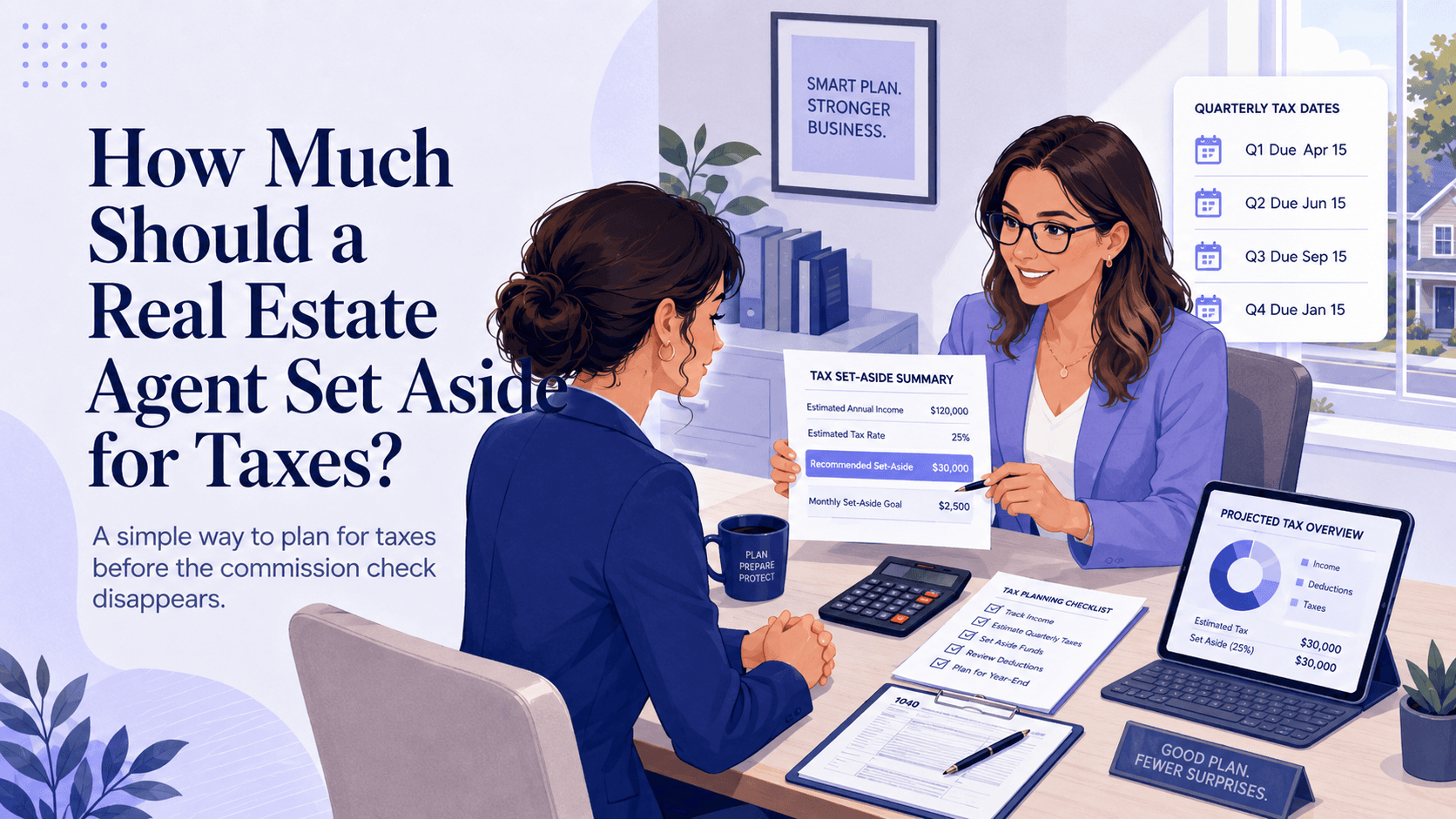

For most real estate agents, a safe starting point is:

25% to 30%

Set aside 25% to 30% of what you keep on every closing, and you will cover most federal and self-employment tax without scrambling in April.

That is not a guarantee. Your exact rate depends on your income, your state, and your deductions. But it is a number that keeps most agents safe instead of sorry.

Why agents owe more than they expect

When you are an employee, taxes come out of every paycheck automatically. As a real estate agent, you are self-employed. Nobody withholds anything for you.

On top of regular income tax, you also owe self-employment tax, which covers Social Security and Medicare. That alone is roughly 15% before income tax even starts.

So the money in your bank account is not all yours. Part of it already belongs to the IRS. You are just holding it.

If you do not set it aside, you will spend money that was never yours to spend.

A simple way to do it

You do not need a complicated system. You need a habit.

Every time a commission check clears:

- Start with what you actually kept after splits, fees, and deal costs.

- Take 25% to 30% of that number.

- Move it into a separate savings account the same day.

- Do not touch it until taxes are due.

Say a closing leaves you with $6,000 after your split and deal costs.

At 30%, you set aside:

$1,800

You live on the other $4,200, and the tax money is already waiting when you need it.

Do that on every deal and tax season stops being an event. It becomes a non-issue.

When to adjust the number

The 25% to 30% range is a starting point. Aim higher if:

- You live in a state with high income tax.

- You are having a big year and crossing into a higher bracket.

- You have few business deductions to offset your income.

You can usually aim lower if:

- You have a lot of legitimate write-offs.

- You file jointly with a spouse who has taxes withheld.

When in doubt, set aside more. Having extra in April is a good problem. Being short is not.

How Kapytl helps

Kapytl keeps a running tax set-aside for you, so you are not doing the math in your head.

As commissions come in and expenses go out, Kapytl tracks what you actually kept and shows a live tax buffer based on it.

You always know two things: how much is safe to spend, and how much is already spoken for.

No spreadsheet. No guessing. No April surprise.